Disaggregation: Silicon’s Advantage

Clayton Christensen, an HBS professor, has a good framework (in The Innovator’s Solution) for thinking about a company’s scope. I’ll give an over-simplified summary of the concept:

In the early days, markets are integrated: The easiest way to solve a new problem is to provide a completely integrated solution. For example, in the early days of the PC industry, the best solutions were provided by companies such as Apple and Silicon Graphics, where they could optimize the software, the hardware, and the market delivery all at once.

As they mature, markets tend to dis-aggregate: As the market matures, tends to dis-aggregate, which allows best-in-class in each category. So Intel can focus on producing good microprocessors, Microsoft can focus on the operating system, and Dell can focus on the assembly & delivery of the PC. All in all, this leads to a better product. By being able to select the best-in-class from each market segment, a customer gets the best possible product.

Clayton Christiansen’s evolution of the PC industry, 1978 – 1990

Source: The Innovator’s Solution, Clayton Christensen & Michael Raynor. Harvard Business School Publishing, 2003

The framework can be useful to look at solar technologies. In particular, let’s contrast the thin film value chain with the silicon value chain.

Thin film: integrated

I’ll use First Solar as the prototype for this segment. (They are being chased by a bunch of startups, but nobody else is manufacturing in the same scale.) They take in a bunch of raw materials: glass, cadmium telluride, and electrical components… and ship out a completed module. Their value chain looks more like Apple’s integrated PC model: they are a single manufacturer responsible for high efficiency, mechanical integrity, and manufacturing uniformity.

Thin Film Value Chain

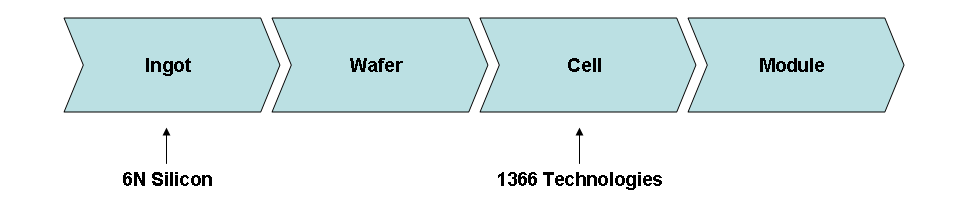

Silicon: disaggregated

The silicon value chain is quite different. There are four discrete pieces of the value chain: silicon is refined into an ingot, then cut into a wafer, then wafers are cut up and scribed to create cells (the step that makes the material photo-active), and then assembled into modules. Each of these products has a market where they can be bought and sold.

Silicon Value Chain

Implications for market competition

Perhaps some of First Solar’s success comes from their close coordination?

Certainly, much of the cost advantage that First Solar enjoys comes from the fact that its semiconductor is thin (and therefore cheap). The bandgap of CdTe is tuned better to the wavelength of the sun’s light. However, their labor content and materials handling costs are also very low, which can only be achieved with the close coordination of manufacturing. Also, by depositing the entire semiconductor stack at once (CdTe, CdS, and the front & back electrodes), First Solar can optimize and minimize the design & materials used.

Silicon might benefit in the longer term from integrating best-in-class technologies across the value chain

Silicon’s value chain should be a long-term strength. Startups can focus on innovating within specific segments of the value chain. They don’t have to integrate vertically in order to produce & ship a product. Therefore, then, the customer will be able to assemble the best-in-class from each market segment, in order to optimize the cost & performance of silicon. A couple examples:

- 6N Silicon is developing technology with uses metallurgical-grade silicon handling for ingot production. Their approach isn’t as pure as the current methods, but the costs fall much faster than the performance does.

- 1366 Technologies is developing technologies to make the cell more efficient: thinner front contacts, a more absorptive front side of the cell, and a more reflective back side.

Both of these startups are focused on different parts of the silicon value chain (ingot and cell, respectively), and so they are not actually competing with each other. Perhaps they might both be part of the winning technology assortment.

So even though First Solar has a huge cost advantage right now, don’t count crystalline silicon out just yet. The market structure is in their favor.

Isn’t the point that in new markets, things will start out vertically integrated, and then as the whole product gets figured out, different companies start to divide up the whole product into logical pieces? If this is true, then one can expect to see that thin film will start to become disaggregated and achieve even better optimizations than where it is now. On the other hand, silicon has already “matured” into the stable, disaggregated state and has wrung out all the advantages that disaggregation brings…

Great question – but thin film (First Solar) actually can’t dis-aggregate. The semiconductor layer is so thin that it must be deposited right on the glass, so you go right from source material to module.

CIGS has a bit more flexibility, since it can be deposited on the back surface rather than the front surface. In other words, it is deposited on a very thin piece of aluminum or stainless steel – which doesn’t by definition then have to be turned into the module. So that would be the middle option: a value chain with two steps (cell and module).

Hi Paul– very interesting set of posts you have up on this blog, thanks.

I wanted to throw in a few other musings about aggregation and disaggregation that I think are relevant:

1. You could extend the value chains you’ve shown to the left, to include things such as sheet glass manufacturing and gas production (thin-film fabs use massive amounts of gases such as N2, H2, SiH4, and so on). Some thin-film and other module factories intentionally build their own glass and gas fabs on-site to simplify logistics and transport, have control over their supply, and I assume capture more of the value chain. This may be a somewhat weak example of aggregation because they may hire glass/gas manufacturers to build these factories rather than building in-house expertise in these established areas– but if so, that’s an example of disaggregation that doesn’t involve physically remote suppliers and increased shipping costs.

2. You could extend the value chains to the right to include mounting systems, trackers, and project development. SunPower is an example of a crystalline silicon company who made a conscious push to aggregate that part of the value chain. I can think of at least two arguments for this. One is that they have an unusually high-efficiency product that can benefit from some custom design in these areas.

The other is that even though the silicon module industry is mature relative to other solar technologies, it’s still been undergoing order of magnitude growth and in some ways is still young, and people who are out there building large projects are still learning about things they can do in the module factory to reduce installation cost.

On the other hand, solar trackers for CPV is an area where many companies are vertically integrated but would love to get out of the business of designing their own trackers, once there are a stable set of proven suppliers they can go to.

3. You could also include manufacturing equipment development in this discussion, though I’m not sure it easily fits on one of those graphs. Many companies with newer technologies (both in thin-film, but also in silicon) develop their own custom manufacturing tools. But this is also an area I’d expect disaggregation to happen as technologies mature (and see for example the AMAT SunFab, though companies that hitched their wagons to that horse may not be doing so well with the competition from higher-efficiency technologies).

Great perspective, Paul. To compare PC’s to Solar technologies is a pretty logical starting point. There is obviously some production restrictions based on the type of panel being produced as to whether a disaggregated model could work, but I would think there is bigger hurdle to overcome: the mass of solar panels. A personal computer, even back in the day of floppy disks and 16 MB RAM, contained a relatively high number of sub-assemblies that could still fit into a box so it could be transported to the next step in the process. Also, because of their size, logistics costs for computer components are a small enough increase (due to high pack density) for the benefit on the piece price (due to specialized suppliers) NOT to be negated, thus creating a benefit of outsourcing sub-assemblies.

I am curious to your take on the implications of increased logistics costs vs. benefits of modular sub-system production efficiencies (and less-quantifiable innovation improvement) in a solar application. Solar panels, though made with similar materials and processes as CPU’s, have a vastly different model when it comes to moving product (sub-assemblies?) between facilities. Or perhaps Solar takes on an automotive model of having “Supplier Parks” located right next the final assembly location. Or maybe the reliability of the system becomes far more important than a lower cost and an Apple-type approach would be superior to a PC-type approach (less factors, less failures). Or maybe there is a way to reduce edge effects and make small, modular panels a practical reality…

Which ever situation plays out, my gut would say that the solar industry is going to have to re-think the traditional high tech/silicon valley production model to deal with the _mass_ the solar panel before a disaggregated model could be realized. But what do you think?

Nick, great thoughts. As far as the bulk of solar modules, it’s definitely true that shipping is a big deal – though it’s really way more relevant for modules than it is for wafers/cells, etc. In fact, I’ll later be devoting an entire post to this, to argue that we can sustain a domestic module manufacturing industry. However, I’m not sure that the shipping costs are a dominant factor in the earlier parts of the silicon value chain.

As far as the tradeoff of shipping costs vs. integration benefits, I don’t know enough about that yet. But the one thing I can say is that small modules don’t make sense – leads to a lot of labor inefficiency on the installation, and drives up the cost of connectors and wiring.

[…] and JA Solar have recently announced a partnership that shows a real-time example of my silicon disaggregation […]