Solar Debate: Power Electronics

This wraps up my “solar debates” series: descriptions of the topics that we debate in the solar industry, at conferences and over drinks. And this last one means a lot to me, because it is the sector that I work in: distributed power electronics.

Introduction

There are plenty of startups working to create better/cheaper/smarter versions of standard solar components – modules, inverters, racking, etc. But there is a category of startups working on technologies that represent a brand new part of the system: smart, module-level electronics.

The basic idea is to put smart boxes behind each solar module. These boxes increase the energy production of the system, and provide data on how each module is performing. To really understand this, it’s worth a quick review of how systems are designed today.

Solar architectures

Currently, an installer will connect all the solar modules (say, 2,000 modules on a commercial rooftop), into an inverter (the size of a small car), which optimizes the power and converts direct current (DC) to alternating current (AC). The problem with this approach is the central ‘optimization.” For example, if the 2,000 modules are not perfectly balanced, then the central optimization won’t be able to get the maximum power. Just a small amount of mismatch can lead to a big drop in power. Also, the system owner doesn’t have any idea what is happening inside the system. The inverter will tell what is happening overall, but doesn’t give any clue what each of the 2,000 modules is doing. If the system doesn’t perform well, it can be very difficult to find the problem.

Category value proposition

This new area has a number of pros, and a couple cons. First, the pros:

Increased energy: By keeping each module performing at its peak power point, these architectures can squeeze more energy out of a solar plant. On a residential system (where there are trees, rooftop obstructions, and other sources of shade), the increased energy could be 10-20%, or even more. On large, unshaded systems, the performance gain is more like 5-7%.

Advanced system data: With these architectures, system owners get data on how each module is performing. A system with 2,000 modules will have 2,000 sources of data, instead of one. This is useful for spotting failures and getting them fixed. Otherwise, small failures can go unnoticed for years. Not only does this keep system uptime higher, but it reduces risk, and therefore should eventually reduce the cost of capital for financing these systems.

Safety: These systems enable plant operators to shut off the power right at the module in the case of an emergency (such as a fire). This makes the rooftops safe for the firefighters to do their jobs.

And, the cons:

Cost: Of course, these systems cost money. The main cost is the cost of the hardware – but customers also factor in the incremental installation cost, if any… and typically the cost of the software.

Efficiency: Any time you have a piece of power electronics in your system, there will be some efficiency loss (even if it is small). So some of the increased energy from the module-level power control is eaten up by the losses from the components in the system.

Risk of failure: Anything can fail. And since these technologies represent a new layer of “stuff”, they also add more potential failure points to the system. This isn’t necessarily fatal – some technologies can fail to the “on” position, where a failure of the electronics won’t stop the module from producing. But it is still a factor.

The Architectures & Startups

A number of startups are all developing slightly different flavors of module-level power electronics. Overall, there are three dominant types:

| Name | Philosophy | Companies |

| Micro-inverter | Take the central inverter, and shrink it down to a much smaller size. Then, put the small inverter on the back of every solar module. | EnPhase

Petra Solar Array Converter |

| DC/DC series | Keep the central inverter, but put a small circuit board on the back of every solar module.

(The modules are still wired in series.) |

Tigo Energy

National Semiconductor SolarEdge Azuray Technology |

| DC/DC parallel (voltage boost) | Keep the central inverter, but put a box on the back of every solar module.

In addition to optimizing the power, the box also boosts the voltage, so each module is wired in parallel. |

eIQ Energy

Tigo Energy |

These innovations create a great arena for debates. Which architectures will win – and how ubiquitous will these components be?

Since I work in this sector, I’m of course biased. So instead of just picking winners, I’ll explain a few of my hypotheses for how this industry will evolve.

1) Micro-inverters do not scale

Micro-inverters do a lot of work (basically, convert DC to AC, and condition it for the grid). But for large systems, it doesn’t make sense to do all of those steps at each module. Many of the components (capacitors, transformers, etc.) are more efficient and cheaper the larger they get. This hypothesis is validated by looking at the costs of the systems: if you compare EnPhase (micro-inverter) to Tigo Energy (DC-DC maximizer), then EnPhase is cheaper for systems under 4kW, and Tigo + central inverter is cheaper for systems above 4kW. Furthermore, the projects validate this: Tigo has recently been installed on a 530kW system on the roof of Clif Bar in Berkeley, while eIQ Energy is developing a 1.8MW system in Southern California.

2) Parallel products have benefits, but come with a cost

Both DC architectures are good, but they have different pros and cons. The series architecture (for example, the Tigo ES Maximizer) has the advantage of being cheaper and more efficient, because it isn’t doing that much work. It’s a “least-intrusive” approach, which keeps the part count really low and the efficiency really high. The parallel approach, on the other hand, is more expensive and less efficient. These products are boosting voltage, often by as much as 10x. So they’re doing more “work.” Now, there are benefits to the parallel design: it’s flexible (for example, can incorporate multiple PV module types into the same inverter), and it offers galvanic isolation, which is safer. And with high-voltage modules (e.g. thin-film), the parallel approach can lead to a significant reduction in copper costs. However, a majority of systems don’t need the benefits of parallel – or, more specifically, the benefits aren’t worth the cost in hardware and efficiency.

3) These architectures can become popular on utility-scale projects, but must prove significant reliability and cost-effectiveness

Within a few years, I believe that module-level power electronics can be popular on the largest solar plants. These projects are much tougher to sell into – the system costs are lower, the profit margins are smaller, and the tolerance for problems (i.e. failures) is far smaller. They are also more likely to use project financing, where large banks have to approve the components – and they typically look for a 5-year track record as a minimum. I think that for module-level power electronics to take off at these systems, they must be very cheap – roughly $0.05/watt or cheaper. But in the next couple years, we can get there. In these systems, the value proposition will be more closely weighted toward data/O&M than simply energy harvest. These systems are managed very aggressively (from a maintenance/uptime point of view), and the module-level data can be hugely helpful to find failures and keep uptime high. The systems will probably drive more financial return from smarter system maintenance than they will from pure energy harvest. Of all of these hypotheses, this one is probably the most controversial – many smart people don’t ever think module-level power electronics belong on large-scale sites. Time will tell.

4) Regulation (particularly safety) can accelerate the adoption

There is growing momentum to make solar systems safer. The best way to do this is to shut off systems at the module-level (other approaches to shutting of a system still leave voltage on the cables, which is not safe at all). So if this keeps moving, we may see these types of architectures essentially mandated by the code/inspector community. The latest development here is the latest edition of the National Electric Code, section 690.11, which basically mandates module-level electronics, and went into effect in January 2011. There are still other things have to happen (including standards for how to test/validate that the equipment works), but this train is already in motion.

5) The data will give early adopters a competitive advantage

Many of the earliest customers of these technologies really see the data as the most important value of the power electronics. I believe that module-level data will become integrated into many aspects of how solar plants are built and managed: how performance is predicted, how the installation & commissioning process works, how the systems are maintained, how warranties are negotiated… and the leading companies will always be one step ahead of their competitors.

(Some brief self-promotion: we’ll be giving a webinar on this in May.)

6) Module-box integration is an important step – but it is a means, not an end

Everyone is watching for the next step of having the electronics integrated into the module to create a “smart module.” Right now these components are installed as separate components, which leads to increased labor and costs. By moving the circuit board into the module, a lot of these costs are eliminated. My only issue with this logic is that a lot of these startups think that their strategy is to exclusively work with module manufacturers. Basically, they want to just convince the module manufacturers to put their products into the modules, and then assume that the volumes will go from $0 to billions overnight. I don’t see the market playing out like that. The module manufacturers first want to see market traction before they will invest in integrating a component. So the startups have to build a solid stand-alone business before they will really be taken seriously by the manufacturers. Also, the module manufacturers won’t necessarily push the new smart module. Once again, the burden will be on the startup to generate the market pull for the product. We’re hoping that Tigo will be the first startup to have a fully-integrated smart module available, hopefully by Q3 of this year.

I love this stuff – this is the most cutting-edge part of the solar sector. And in the next couple years, my hypotheses will be proven or disproven. Stay tuned – in the meantime, I’ll share news below:

3/18/2011: A literal debate on this topic, last week

2/24/2011: More startups entering the market

1/20/2011: A nice profile of Tigo Energy

12/28/2010: Power electronics – #7 on the year in review

Five Solar Debates: the Efficiency Race

CdTe and CIGS are the two new kids on the block for thin-film solar. Both technologies promise rock-bottom manufacturing prices, and respectable efficiencies (10% or greater). First Solar’s CdTe modules have given them a $10Bn market cap and pole position in the industry, while a number of high-flying CIGS and CdTe startups chase them.

First Solar may have all the manufacturing scale, but there is still a measure on which these technologies are still competing very closely: efficiency. Higher efficiencies are huge because the same amount of glass & aluminum provides more power – and since modules are priced based on their power, that extra money goes straight to the bottom line of the manufacturer.

Bandgap background

To understand what will determine efficiency, we have to dive into physics for a moment. I’ll keep it quick. Photons from the sun come in a wide range of wavelengths – this is what gives us the color spectrum.

Solar Spectrum

So the solar cells are tasked with absorbing that spectrum of light. Ideally, they would absorb the entire spectrum – but in reality, there are a host of constraints (e.g. shading, reflection, and recombination) that reduce the amount that a cell can absorb.

Source: Newport Spectra-Physics GmbH

CdTe and CIGS have been selected because their bandgap efficiency is very good, so a very thin layer can capture much of the sun’s energy. This is where they get the name “thin film.” (One interesting thing in the chart below: notice how the thinner CdS layer (which is physically in front of the CdTe) improves the cell efficiency. This illustrates the shading phenomenon – just a small taste of what the folks at First Solar and Abound are working on…)

CdTe efficiency spectrum, from Reuben Collins

What is efficiency, anyway?

You might be asking what “10% efficiency” means. It’s actually way simpler than you think. “Full sunlight” (noon on a summer day), means that a square meter of earth at sea level is hit with 1,000 watts of energy. A nice round number. So to put it mathematically, a full sun is equal to 1kW / m^2.

Efficiency is therefore a measure of the amount of sunlight that a module can absorb at full sun. A 10% efficient module that is exactly 1 square meter large would generate 100W in full sun (1,000W x 0.10). Using real numbers: a First Solar module is 1.2m x 0.6m (0.72 square meters). If it generates 80 watts at peak power, that module is 11.1% efficient (80W/(0.72 square meters*1000)).

The Debate

The efficiency race between these two technologies has been close for decades (see the chart below). Both have a theoretically maximum efficiency of about 30%. CIGS advocates brag that CIGS has the highest lab efficiency (19.9% efficient). However, it was done using an intensely complex process: quadruple sublimation (essentially, evaporating four different components at the same time, at very precise levels). This process was so complex, in fact, that no company is seriously trying to commercialize it.

CdTe has a lower champion cell, but it is much simpler to manufacture. Its bandgap (1.4 eV) is almost perfectly tuned to capture the most sun with the least material.

Champion cell, CIGS vs. CdTe (with a-Si pulling up the rear)

[Again, a disclaimer: I used to work at a CdTe startup.]

So what do the companies have to say? What is being produced out of real factories? We can look at available datasheets to see the efficiencies promised:

| Company | Material | Size | Power | Efficiency |

| First Solar | CdTe | 0.72 m^2 | 70W – 80W | 9.7% – 11.1% |

| Nanosolar | CIGS | 2.0 m^2 | 160W – 220W | 8.0% – 11.0% |

| Wurth | CIGS | 0.73 m^2 | 70W – 80W | 9.6% – 11.0% |

| Solyndra | CIGS | 1.97 m^2 | 150W – 200W | 7.6% – 10.2% |

| Stion | CIGS | 1.10 m^2 | 110W – 130W | 10.0% – 11.8% |

Pretty close, huh? That’s why it’s still an open debate. Physicists tend to predict that CIGS will eventually win – the lab efficiency is so much higher! But manufacturers have a healthy respect for the simplicity of CdTe; First Solar may keep the thin-film efficiency crown for years to come, through their manufacturing prowess. And only time will tell.

One last caveat on cell efficiency: don’t mistake cell efficiency for module efficiency. Module efficiency is always lower – often by 10-20%. (An analogy: cell efficiency is sort of like highway MPG, whereas module would be city MPG.) There are a bunch of reasons for this difference: resistance in the module, mismatch across cells, or shading from the front electrodes. Cell efficiency is still important – but module efficiency is what you’ll actually get in the real world.

Five solar debates: will a-Si and Concentrating PV survive?

[PS: sorry for the silence the last couple weeks. Prep for Intersolar was pretty intense. Great show, though.]

Radical solutions to the efficient frontier

I’m a big fan of the efficient frontier framework in solar: in general, you can get better performance, but you have to pay more. And while everyone wants to break away from the pack, most people who claim to be way off from the efficient frontier are lying to themselves.

There are two technologies that have taken new approaches to the efficient frontier: amorphous silicon (low cost, low efficiency), and concentrating PV (high efficiency, but higher system cost). Neither approach is guaranteed to pay off. I’ll break down the outlook on both.

Efficient Frontier in Solar PV

Amorphous Silicon

Life…

The amorphous silicon market is dominated by two tool major manufacturers, Applied Materials and Oerlikon. They have, collectively, nearly a dozen clients, including ENN, Signet Solar, Sunfilm and Moser Baer.

There are also a number of large companies with amorphous products as part of their portfolio, such as Sharp, DuPont, and Q-Cells/Sontor. Sharp’s business seems to be thriving. Even Qualcomm is getting into the mix.

Seems like a nice list of blue-chip clientele.

…Or Death?

However, the technology already has a few black eyes. Sunfilm filed for bankruptcy, and eventually merged with Sontor. Applied Materials is rumored to be scaling back their business, and considering abandoning it. This is led some people to question whether this technology will even become obsolete. Part of the problem is that amorphous’ low efficiency forces them to pay a penalty, as I explain here.

Concentrating Solar (PV)

Concentrating PV is also controversial. They start with high-efficiency semiconductors (efficiency of nearly 40%) which are very expensive. Since the material is expensive, they shrink it reduce the cost, and use lenses to concentrate the light that it sees. Most concentration factors range from 10x to 500x – meaning that you use 10x to 500x less material, and that material would see 10 to 500 times the regular intensity of the sun.

However, the decision to use concentrators creates other system requirements. The optical systems require the lens to be pointed at the sun (in other words, dual-axis trackers are required). These are expensive. Also, that much concentration generates a ton of heat – so these systems typically incorporate a cooling system. Again, more cost.

Life…

The sector has a number of well-funded, talented startups, including SolFocus, GreenVolts, Solar Junction, Solaria and Soliant. Amonix just closed a 126MM round from Kleiner Perkins and Goldman Sachs – smart money, a very good sign for the sector.

…or Death?

On the other hand, the market has over-promised and under-delivered for years. There are still big detractors, and I’ve heard someone within the industry say that if they don’t put up big numbers in 2010, they never will. Finally, there are a lot of questions about the long-term maintenance requirements of the systems, and these questions won’t be answered conclusively for years.

My call

I think both of these technologies have legs, particularly in specific applications. Amorphous can thrive in large applications where the economics are in their favor, while concentrators are great in areas with a lot of direct sun. But the jury is out on whether these will remain niche technologies or serious players.

What do you all think? Either way, we can follow the news below (and keep checking back for updated stories/links):

Recent amorphous news

7/21/10: What timing! AMAT will no longer sell SunFab

7/15/10: Oerlikon boasts of new customers and higher efficiencies

7/14/10: Sharp claims a-Si will constitute half of their business

6/9/10: Signet Solar appears to be insolvent

5/19/10: Reports that AMAT will redesign their Sunfab, and potentially abandon the business

4/2/10: Bankruptcy for Sunfilm/Sontor

2/4/10: Nice in-depth analysis of the a-Si market

Recent CPV news

7/13/10: Concentrix announces plans for 1MW site in NM, and SolFocus claims LCOE of $0.085

4/21/10: Amonix raises 130MM from Kleiner, Goldman Sachs

6/18/09: Greenvolts coverage, with some criticism of the sector

Innovalight Case Study

(A quick interruption of the solar debates series – I’ll return to it with the next post. But I wanted to comment on some breaking news.)

Innovalight and JA Solar have recently announced a partnership that shows a real-time example of my silicon disaggregation thesis.

A quick background: Innovalight is a startup that is developing a quantum dot ink. Quantum dots are basically nano-sized particles that capture a very specific wavelength of light, depending on their size. So these inks can be tuned (simply by controlling their size) to capture extra light beyond the spectrum that a normal solar cell collects. It’s like a little booster layer that captures more light.

Pretty sexy science. But what I like even more is that they can deposit their ink using standard printing tools, and integrate this into existing production lines. (And if, as they claim, it only requires a single step, this implies that there are no other chemical, thermal, or drying steps required.) So Innovalight doesn’t have to be in the cell manufacturing business. That’s where JA Solar (a top-5 Chinese solar cell manufacturer) comes in.

Pretty sexy science. But what I like even more is that they can deposit their ink using standard printing tools, and integrate this into existing production lines. (And if, as they claim, it only requires a single step, this implies that there are no other chemical, thermal, or drying steps required.) So Innovalight doesn’t have to be in the cell manufacturing business. That’s where JA Solar (a top-5 Chinese solar cell manufacturer) comes in.

From JA Solar’s point of view, this ink can be a huge win. If, as the article claims, they can transform a 30MW line to a 35MW line, this represents a 14% reduction in cost, both for their cost of goods (because the same physical module produces more power), and for their CAPEX/watt (because the same production line can be amortized over more power produced). Of course, this is before factoring in the cost of the ink and printing equipment – and there are likely other technical challenges that I won’t get into here.

But most important, in my opinion, is what this signals for the silicon value chain. Inks could represent one more piece of the market. There will be competition – perhaps Innovalight will remain dominant, but maybe not. But either way, silicon modules can assemble the best in class from each of these sub-markets – wafers, cells, inks, etc – and that is good for getting costs down and performance up.

And this competition is something that the monolithically-integrated thin-film players don’t get to benefit from.

Five Solar Debates: the Thin-film Race

These are exciting times for the solar industry. There has been a ton of innovation, a ton of investment, and it’s finally time to see who can make good on their promises. But many of the best competitions require an insider’s understanding of the industry. I’m going to try to change that.

This is the beginning of a five-post series where I will frame some of the key battles that are playing out right now in the solar industry. Almost like a scouting report for a football game. And the first topic is:

The Thin-film Horse Race: Who will emerge first to challenge First Solar?

The debate

Thin-film solar modules are dramatically cheaper than silicon modules. You only need to look at First Solar’s numbers (costs under $0.90/watt) to see the proof. However, they are challenging to manufacture. There have been six thin-film startups (see table below) that have raised over $100MM in venture funding, assembled world-class management teams, and still have not yet been able to ramp up their manufacturing facilities. But they are close. So the question is: which company will figure it out first?

This is actually a battle of manufacturing technologies:

| Company | Manufacturing Technology | Investors |

|

|

Thermal Sublimation | Doll Capital Management, Technology Partners, GLG Partners, The Invus Group |

|

|

Field-Assisted Simultaneous Synthesis and Transfer (basically, evaporating two films, and then sandwiching them together) | NEA, Morgan Stanley, Noventi Ventures, Paladin Capital Group, Yellowstone Capital, Sequel Venture Partners |

|

|

Sputtering | Kleiner Perkins, Firelake Capital, Vantage Point, Atel Ventures, Bessemer, Leaf Clean Energy, Atlas Venture, Garage Technology Ventures, Passport Capital |

|

|

Ink Deposition | Mohr Davidow, Firelake Capital, Capricorn, U.S. Venture Partners, Benchmark Capital, Riverstone Holdings, The Carlyle Group |

|

|

Electroplating | Crosslink Capital, Hudson Clean Energy, Musea Ventures, Firsthand Capital, Convexa Capital |

|

|

Ink Deposition | RockPort Capital, CMEA, U.S. Venture Partners, Virgin Green Fund, Argonaut Private Equity, Redpoint Ventures |

What will determine the winners?

The key to winning this race is all about “manufacturability”: the ability to deposit a very thin semiconductor with complete uniformity, and then repeat that a million times, so that the millionth looks just like the first. This is way harder than it seems: materials build up on the equipment, small errors compound into big ones, and things that should be repeatable are never that easy.

Also, there is a big difference between having the capacity and having a running production line. It only takes money to buy the equipment, but it takes a lot of good engineering to get it running well.

So ultimately, these companies are constrained by their ability to manufacture, more than their customers’ willingness to buy their products.

Success is subjective, but I define it as manufacturing at a 100 megawatt-per-year run rate. In comparison, First Solar recently crossed the 1 gigawatt (1,000 megawatts) capacity mark.

My opinion

This is a common debate among solar followers, and nobody know who will emerge first. I think Miasole and Abound are at the head of the class, and closest to scaling to 100MW and beyond. [Note: I used to work at Abound, so I may be biased.] This is a slight underdog pick, as Solyndra and Nanosolar have more money and higher profiles. Think of it as the NY Yankees (Solyndra) versus the Tampa Bay Devil Rays (Miasole & Abound): they are close, in spite of having a smaller budget. Ultimately, time will tell who wins.

In the meantime, I’ll keep posting news stories below so we can all watch as these companies scale up. Check back from time to time, as I’ll keep posting relevant news.

News:

Miasole: 22MW expected shipments in 2010, 6/10/2010

Abound Solar: 24-30MW run rate, off a line with 65MW capacity, 5/21/2010

Miasole: fab (at full uptime) has capacity of 75MW, 5/12/2010

Nanosolar: 640MW capacity in Germany (but no claims of running the line), 3/22/2010

SoloPower: working on a 60MW fab, which will be producing in 2011, 2/18/2010

HelioVolt: fab will have 20MW capacity (no guidance on timing, though), 1/7/2009

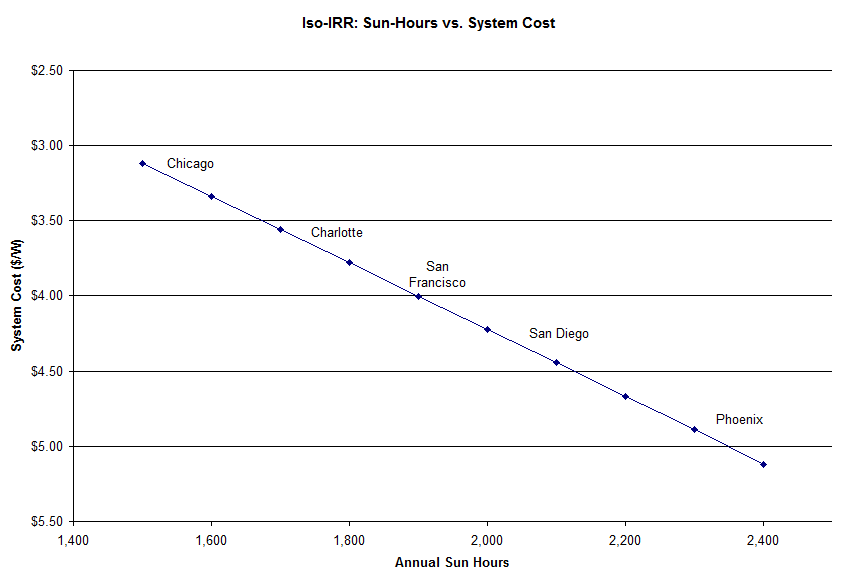

Iso-IRR pt 3: Sunlight

The Iso-IRR curve seems to be a popular way to think about different solar plants. So I wanted to use it to look at how much sun matters.

Turns out it matters a lot. As a location’s sunlight goes up, so does a developer’s willingness to pay for it. That’s not a big surprise. What I do find surprising is the overall magnitude of the impact. A developer in Phoenix would be willing to build a solar plant for roughly $1.75 more per watt (with the same return) than an identical system in Chicago – a 57% premium.

This is why people expect the most promising American solar development to take place in the sunny southwest. And reinforces how impressive Germany’s support of the industry has been (their sunlight resembles Chicago’s).

Final technical notes:

The model behind this is the same LCOE model that I posted a couple weeks ago (I used model #3). Keep in mind that, as always, the exact numbers are not precise, use this only directionally.

Also, the sun-hour per city data comes from NREL. For now, I have been using full-tilt sun data (with the module tilt equal to the location’s latitude), but in future posts I’ll look at how this changes with lower tilt.

Burdened LCOE

Renewable energy isn’t yet competitive with the grid. That’s no surprise. However, it’s an unfair fight. And I’m not talking about carbon pricing (which would be nice). I’m talking about the fact that renewables will deliver energy, with zero fuel costs, for 20-25 years, while they are being compared against today’s spot price for electricity. And while electricity prices may change, the energy out of a solar project is locked in as soon as you build it. In other words, renewable energy plants provide a hedge against future energy price changes.

And electricity prices have a good chance to increase in the future. Historically, they have grown by about 2% per year, but many smart people think they will grow at faster rates going forward.

That benefit is hard to bake into today’s current LCOE calculations. But if the price of electricity is rising, then the true comparison for a renewable source is not today’s price, but the average electricity price over the next 25 years.

I’ve created a metric called “Burdened LCOE”. For this, I’m simply starting with today’s energy rates, and then growing them over 25 years, at different growth rates. The 25-year average is the burdened LCOE.

Burdened LCOE, as function of growth rate

The impact is significant. A customer paying $0.15/kWh today would actually have a burdened 25-year LCOE (with 4% annual price growth) of $0.25/kWh. In other words, someone would be just as well-off by buying a solar system with a $0.25 LCOE as they are if they pay $0.15 today, expecting prices to go up by 4% per year. Someone paying $0.12 today would expect to pay an average of $0.20 over the same horizon. Seen through this lens, renewables are much more competitive with fossil fuels.

So this begs the question: will electricity price increases actually accelerate? I don’t know. But many of the smartest people are betting on this. Some reasons to be bullish on electricity prices:

- Natural gas prices may increase. We have a lot of supply, but limited refining capacity and port capacity for importing LNG. That’s the extent of my knowledge – for people who know what they are talking about, surf over to The Oil Drum.

- Coal plants are not being built. Activism and NIMBYism are preventing nearly all new coal plants from being built. See Earth2Tech’s coal death map. So supply of electricity cannot keep up with demand. Prices rise.

- Maintenance costs will likely go up. This is related to the fact that no new plants are built – therefore, old plants have to be kept running beyond their planned lifetimes. Maintenance costs begin to escalate.

Look, I’m not trying to convince you to buy electricity futures. But I am trying to get you to cut renewables some slack when comparing a 25-year generation asset against an electricity spot price that may go up tomorrow.

Demystifying LCOE

(Quick caveat: this article is meant for beginners who are unfamiliar with LCOE. To those in the industry, this will be too basic. I’ll have another post for insiders soon – a new metric I call “Burdened LCOE”.)

Levelized Cost of Electricity (LCOE) is a valuable metric. LCOE allocates the costs of an energy plant across its useful life, to give an effective price per each unit of energy (kWh). In other words, it’s like averaging the up-front costs across production over a long period of time.The nice thing about LCOE is that it gives a single metric that can be used to compare different types of systems – from renewable projects, where the up-front capital cost is high and the ‘fuel’ cost is near zero, to a natural gas plant, where the capital cost is lower, but the fuel cost is higher. And it can even be compared against the price you pay on your utility bill ($/kWh).

However, LCOE is also feared – mainly because it can be complex. I’m going to try to change that here.

Instead of just giving a single overview of an LCOE model, I’m going to show a few different levels of detail, so you can matches the level of model complexity with what you’re trying to accomplish. You can follow along by downloading the model “Simple LCOE x3” from the box.net sidebar.

Level 1: Back of the Envelope: This is minimum amount of analysis needed to get to a number that even looks like an LCOE. You only need four numbers:

- System size: This is often referred to as the ‘nameplate capacity’ of the system. Specifically, it is a measure of how much power the system could produce when running at full strength.

- System cost: The cost to install the system – most often given on a per-watt basis. For example, if you get a quote for someone to build a 10kW (10,000 watts) nameplate system for $40,000, that is a cost of $4/watt.

- Watt-hours per watt-peak: The nameplate power is only half of the story: you then need to know how much energy you get out (power delivered over a period of time). So this number measures how many hours per year the system is operational – in other words, how many hours of sun does a system receive.

- Productive years: Since the production happens over time, it’s critical to understand how many years the system will work. Most components are warranted for 20-25 years.

Level 2 – If you want to include all assumptions that are significant, you need three more:

- Nameplate de-rating: Even if a system is supposed to produce 10,000W, it rarely produces that. There are a lot of steps in processing the power (efficiency losses in the inverter, wire, and other operation), and they eat up about 20% of the power between the module and the grid.

- Discount rate: future value is discounted against today’s. Otherwise, you could invest your money today, get a return, and then invest a larger amount tomorrow. For the purposes of an LCOE, I discount future production – which accomplishes the same goal.

- Incentives: whether we like it or not, government incentives matter. At the federal level, there is a 30% tax credit (refunds 30% of the system cost). There are also dozens of state and municipal incentives (the best summary is www.dsireusa.org).

Level 3 – Three more variables will make you sound more credible when talking to people in the industry:

- Degradation: Systems degrade over time – and this includes the PV modules themselves. Most assume that degradation is between 0.5% and 1% per year. Note that most modules are warranted to perform up to 90% of their rated power for 10 years, and 80% of their rated power for 25 years – numbers that aren’t far off from 1% annual loss.

- Maintenance: Someone has to clean the modules and repair the broken units. This is often modeled as a percent of the initial cost (typically about 0.5%), recurring every year.

- Inverter replacement: Unfortunately, most inverters need to be replaced. While reliability is improving, most people assume that the inverter will have to be replaced at about year 10.

In the box.net sidebar, I’ve uploaded a model (“Simple LCOE x3.xls”) that has all three of these models. Feel free to download and use freely.

Also, if you want to learn more about each of the assumptions, here is a summary of typical ranges, with further reading where possible:

| Metric | Low value | Average value | High value | Further information |

| System Cost ($/watt) | Residential: $5.00

Commercial: $4.00 Utility-scale: $3.00 |

Residential: $6.00

Commercial: $5.00 Utility-scale: $4.00 |

Residential: $7.00

Commercial: $6.00 Utility-scale: $4.50 |

|

| Watt-hours per watt-peak | 1,400-1,600 | 1,700 – 1,900 | 2,000-2,200 | http://rredc.nrel.gov/solar/old_data/nsrdb/redbook/ |

| Time horizon | NA | 20 years | 25 years | |

| De-rating | 77% | 80-82% | 85% | PVWatts model from NREL: http://rredc.nrel.gov/solar/calculators/PVWATTS/version1/derate.cgi |

| Discount rate | 7-8% | 9-12% | 13-15% | Ask a banker |

| Incentives | 30% Federal Tax Credit | DSIRE (Database of State Incentives for Renewable Energy): http://www.dsireusa.org/ | ||

| Degradation | 0.25% | 0.5% | 0.75% | |

| Maintenance | 0.25% | 0.5% | 0.75% | |

| Inverter replacement year | 7 | 10 | 15 | |

| Inverter replacement cost ($/watt) | $0.30 | $0.35-$0.45 | $0.55 |

Finally, keep in mind that the variables above still leave out a ton of complexity. The system cost depends on hundreds of design decisions; the solar module’s production depends on its tilt angle and temperature (among other things). But if you’re starting from scratch, this is a good place to start.

Update, June 6: I’ve fixed a bug in the LCOE model. (I wasn’t discounting the inverter replacement in model #3.)

//

CIGS’ Complexity Paradox

Thin-film solar research is largely a two-party system. Its two dominant ideologies are cadmium telluride (CdTe) and copper indium gallium (di)selenide (CIGS), the two different semiconductors used as the active PV layer. And like politics, you can find people who argue the merit of each side – sometimes, beyond the point of reason.

Both technologies have loads of promise: module efficiencies upwards of 15+%, and costs of around $0.50/watt. But the similarities end there.

Supporters of CIGS point to its versatility (can be manufactured in dozens of ways, including methods at room temperature and room pressure), and its higher theoretical efficiency (its bandgap physics is better, plus the highest CIGS cell efficiency is 20.1%, while CdTe is 16.5%).

Supporters of CdTe point to its simplicity – the active layer requires just two components (CdS and CdTe), which are deposited right next to each other… while CIGS actually requires at least six components (C, I, G, S, plus Sodium, Sulfur, and CdS) in a much more complex configuration. Oh, and the CdTe camp has First Solar: the powerhouse with a multi-billion backlog, 1GW of production capacity, and gross margins north of 40%, even in a horrible solar market.

So if these technologies are both legit, then why the imbalance in venture capital funding:

| Thin-film startups that have raised $100MM+ in the last ~4 years: | |

| CIGS | Cadmium Telluride |

| Heliovolt | Abound Solar |

| Miasole | |

| Nanosolar | |

| SoloPower | |

| Solyndra | |

(You could also set the bar lower (e.g. startups to raise $20MM+), and the list would look similar (add Stion to the CIGS side). And I’ve heard anecdotally from VCs that the number of business plans that went unfunded had a similar bias toward CIGS.) So how did CIGS get so much more money, while CdTe has the only ‘victory’ (FSLR) to date?

One Theory

Recall the point I made above: CIGS is way more complex (six or more components), and it is way more versatile in how it can be deposited (ink deposition, electroplating, sputtering, chemical vapor deposition, etc). Now, put yourself in the shoes of a materials science PhD candidate at Stanford, or a researcher at NREL. Which semiconductor would you study? There are probably 10x more ‘interesting’ problems on the CIGS side. And in general, an interesting problem leads to an interesting solution, which leads to getting published.

Continuing this logical chain… CIGS gets more research, therefore more CIGS patents are filed. More companies are founded around CIGS, and more talented management teams are built around CIGS. Ultimately, this would lead to more VC money flowing to CIGS.

The Implication

The thing I find most interesting, if this is correct (with stress on the “if”): it illustrates a direct conflict between the academic research community and the venture capital community – groups which otherwise have a very symbiotic relationship. Academia is pulled toward complexity, because that presents more novel research topics. However, for commercialization, simplicity is likely to be more profitable than complexity.

This may be changing. The venture and research communities learn quickly, and all the companies above were funded circa 2005-2009. Sequoia’s more recent investment into SunPrint is a small signal of the increased focus on simplicity & manufacturability.

Final notes:

- Apologies to the amorphous silicon crowd for not including you in the ‘thin-film research’ category. But my focus here is on academic research and venture funding, where I haven’t seen a-Si being actively pursued with the same vigor.

- Anyone have any ideas for data I could find to test this hypothesis? Besides simply counting patents, is there any good way to track the papers published, by type of semiconductor?

- A request to those who are well-versed in fuel cells or electrochemical batteries – could this same phenomenon be playing out in those markets? Are complex technologies getting disproportionate funding?

Trackers are an endangered species

Trackers are becoming rare in most solar projects. The common wisdom, which just about anyone in the industry will say, is that dropping module prices make it difficult for trackers to compete. I decided to model this, to confirm quantitatively that it is true.

Fundamentally, trackers improve the performance of solar plants by keeping the solar modules aligned with the sun. At the highest level, there are two types of trackers: single-axis trackers (rows of modules pivoting along a bar), and dual-axis trackers, where a block of modules rotates in every direction. (See pictures of examples below.) In general, a single-axis tracker will increase a system’s energy production by about 25%, while a dual-axis tracker will increase production by about 35%.

Single-axis tracker

Dual-axis tracker

So why aren’t trackers used more often, if they can increase production? Again, this can be shown with a simple model. In this model, I am dramatically over-simplifying a solar system, to show only the installed cost per watt, versus the total energy production per watt. The only variable that I’m changing is the system cost – and then adding a tracking system.

Single-axis tracker model

A tracker changes the system in two ways: it adds a fixed cost (in $/watt), and increases production by a percentage. Given these assumptions, you can see that a dropping system cost makes trackers less attractive. What’s interesting is that the drop in ROI actually accelerates as systems get cheaper:

Tracker ROI

There is some intuition for this. Think of a tracker as a product which ‘extends’ the power production of a system. But when the system gets cheap enough, it becomes more cost-effective to simply extend the system by installing more solar modules and ditching the tracker.

Finally, I want to explain why SunPower is still using trackers today (correctly). First, they are more expensive, so they tend to be on the left side of the chart above. But they also have the highest power density – so the tracker is actually slightly cheaper on a $/watt basis. The same amount of tracking hardware moves more watts. (I chose not to model the power density in the exercise above, because it made the model much more complex, and therefore more difficult to explain.)

End Notes & Disclaimers:

All of the costs here (including system and tracker cost) are approximate. But again, the fundamental relationship (lower PV costs lead to lower tracker ROI) will be the same.

Also, a big omission here is the time value of money: I’m not discounting future production (since, of course, you pay for a system up front, while the production is later on). This will make the trackers look worse across the board. Like the module efficiency, the time value of money is something that adds a lot of complexity, but doesn’t change the point.

Finally, this entire discussion only applies to flat-plate solar modules. For concentrating solar PV, tracking is an absolute requirement at any cost.

11 comments