Innovalight Case Study

(A quick interruption of the solar debates series – I’ll return to it with the next post. But I wanted to comment on some breaking news.)

Innovalight and JA Solar have recently announced a partnership that shows a real-time example of my silicon disaggregation thesis.

A quick background: Innovalight is a startup that is developing a quantum dot ink. Quantum dots are basically nano-sized particles that capture a very specific wavelength of light, depending on their size. So these inks can be tuned (simply by controlling their size) to capture extra light beyond the spectrum that a normal solar cell collects. It’s like a little booster layer that captures more light.

Pretty sexy science. But what I like even more is that they can deposit their ink using standard printing tools, and integrate this into existing production lines. (And if, as they claim, it only requires a single step, this implies that there are no other chemical, thermal, or drying steps required.) So Innovalight doesn’t have to be in the cell manufacturing business. That’s where JA Solar (a top-5 Chinese solar cell manufacturer) comes in.

Pretty sexy science. But what I like even more is that they can deposit their ink using standard printing tools, and integrate this into existing production lines. (And if, as they claim, it only requires a single step, this implies that there are no other chemical, thermal, or drying steps required.) So Innovalight doesn’t have to be in the cell manufacturing business. That’s where JA Solar (a top-5 Chinese solar cell manufacturer) comes in.

From JA Solar’s point of view, this ink can be a huge win. If, as the article claims, they can transform a 30MW line to a 35MW line, this represents a 14% reduction in cost, both for their cost of goods (because the same physical module produces more power), and for their CAPEX/watt (because the same production line can be amortized over more power produced). Of course, this is before factoring in the cost of the ink and printing equipment – and there are likely other technical challenges that I won’t get into here.

But most important, in my opinion, is what this signals for the silicon value chain. Inks could represent one more piece of the market. There will be competition – perhaps Innovalight will remain dominant, but maybe not. But either way, silicon modules can assemble the best in class from each of these sub-markets – wafers, cells, inks, etc – and that is good for getting costs down and performance up.

And this competition is something that the monolithically-integrated thin-film players don’t get to benefit from.

Five Solar Debates: the Thin-film Race

These are exciting times for the solar industry. There has been a ton of innovation, a ton of investment, and it’s finally time to see who can make good on their promises. But many of the best competitions require an insider’s understanding of the industry. I’m going to try to change that.

This is the beginning of a five-post series where I will frame some of the key battles that are playing out right now in the solar industry. Almost like a scouting report for a football game. And the first topic is:

The Thin-film Horse Race: Who will emerge first to challenge First Solar?

The debate

Thin-film solar modules are dramatically cheaper than silicon modules. You only need to look at First Solar’s numbers (costs under $0.90/watt) to see the proof. However, they are challenging to manufacture. There have been six thin-film startups (see table below) that have raised over $100MM in venture funding, assembled world-class management teams, and still have not yet been able to ramp up their manufacturing facilities. But they are close. So the question is: which company will figure it out first?

This is actually a battle of manufacturing technologies:

| Company | Manufacturing Technology | Investors |

|

|

Thermal Sublimation | Doll Capital Management, Technology Partners, GLG Partners, The Invus Group |

|

|

Field-Assisted Simultaneous Synthesis and Transfer (basically, evaporating two films, and then sandwiching them together) | NEA, Morgan Stanley, Noventi Ventures, Paladin Capital Group, Yellowstone Capital, Sequel Venture Partners |

|

|

Sputtering | Kleiner Perkins, Firelake Capital, Vantage Point, Atel Ventures, Bessemer, Leaf Clean Energy, Atlas Venture, Garage Technology Ventures, Passport Capital |

|

|

Ink Deposition | Mohr Davidow, Firelake Capital, Capricorn, U.S. Venture Partners, Benchmark Capital, Riverstone Holdings, The Carlyle Group |

|

|

Electroplating | Crosslink Capital, Hudson Clean Energy, Musea Ventures, Firsthand Capital, Convexa Capital |

|

|

Ink Deposition | RockPort Capital, CMEA, U.S. Venture Partners, Virgin Green Fund, Argonaut Private Equity, Redpoint Ventures |

What will determine the winners?

The key to winning this race is all about “manufacturability”: the ability to deposit a very thin semiconductor with complete uniformity, and then repeat that a million times, so that the millionth looks just like the first. This is way harder than it seems: materials build up on the equipment, small errors compound into big ones, and things that should be repeatable are never that easy.

Also, there is a big difference between having the capacity and having a running production line. It only takes money to buy the equipment, but it takes a lot of good engineering to get it running well.

So ultimately, these companies are constrained by their ability to manufacture, more than their customers’ willingness to buy their products.

Success is subjective, but I define it as manufacturing at a 100 megawatt-per-year run rate. In comparison, First Solar recently crossed the 1 gigawatt (1,000 megawatts) capacity mark.

My opinion

This is a common debate among solar followers, and nobody know who will emerge first. I think Miasole and Abound are at the head of the class, and closest to scaling to 100MW and beyond. [Note: I used to work at Abound, so I may be biased.] This is a slight underdog pick, as Solyndra and Nanosolar have more money and higher profiles. Think of it as the NY Yankees (Solyndra) versus the Tampa Bay Devil Rays (Miasole & Abound): they are close, in spite of having a smaller budget. Ultimately, time will tell who wins.

In the meantime, I’ll keep posting news stories below so we can all watch as these companies scale up. Check back from time to time, as I’ll keep posting relevant news.

News:

Miasole: 22MW expected shipments in 2010, 6/10/2010

Abound Solar: 24-30MW run rate, off a line with 65MW capacity, 5/21/2010

Miasole: fab (at full uptime) has capacity of 75MW, 5/12/2010

Nanosolar: 640MW capacity in Germany (but no claims of running the line), 3/22/2010

SoloPower: working on a 60MW fab, which will be producing in 2011, 2/18/2010

HelioVolt: fab will have 20MW capacity (no guidance on timing, though), 1/7/2009

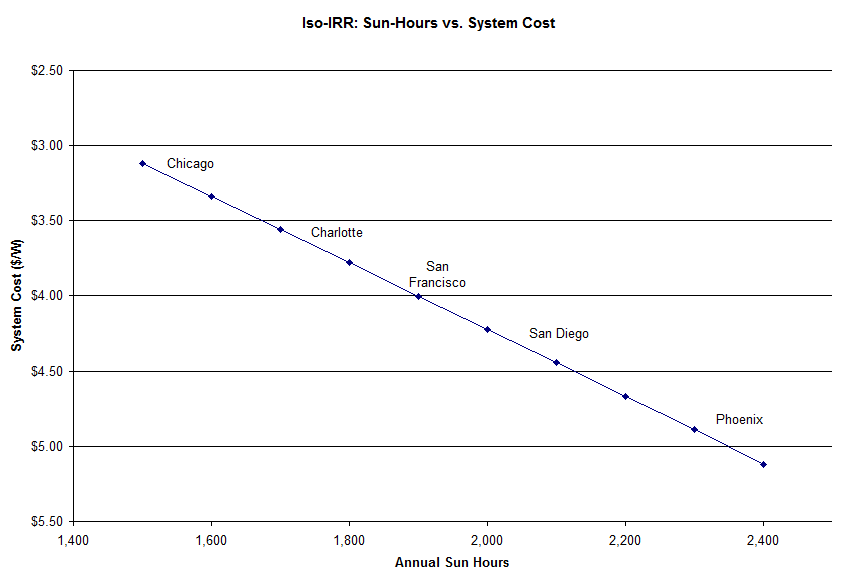

Iso-IRR pt 3: Sunlight

The Iso-IRR curve seems to be a popular way to think about different solar plants. So I wanted to use it to look at how much sun matters.

Turns out it matters a lot. As a location’s sunlight goes up, so does a developer’s willingness to pay for it. That’s not a big surprise. What I do find surprising is the overall magnitude of the impact. A developer in Phoenix would be willing to build a solar plant for roughly $1.75 more per watt (with the same return) than an identical system in Chicago – a 57% premium.

This is why people expect the most promising American solar development to take place in the sunny southwest. And reinforces how impressive Germany’s support of the industry has been (their sunlight resembles Chicago’s).

Final technical notes:

The model behind this is the same LCOE model that I posted a couple weeks ago (I used model #3). Keep in mind that, as always, the exact numbers are not precise, use this only directionally.

Also, the sun-hour per city data comes from NREL. For now, I have been using full-tilt sun data (with the module tilt equal to the location’s latitude), but in future posts I’ll look at how this changes with lower tilt.

leave a comment