Disaggregation: Silicon’s Advantage

Clayton Christensen, an HBS professor, has a good framework (in The Innovator’s Solution) for thinking about a company’s scope. I’ll give an over-simplified summary of the concept:

In the early days, markets are integrated: The easiest way to solve a new problem is to provide a completely integrated solution. For example, in the early days of the PC industry, the best solutions were provided by companies such as Apple and Silicon Graphics, where they could optimize the software, the hardware, and the market delivery all at once.

As they mature, markets tend to dis-aggregate: As the market matures, tends to dis-aggregate, which allows best-in-class in each category. So Intel can focus on producing good microprocessors, Microsoft can focus on the operating system, and Dell can focus on the assembly & delivery of the PC. All in all, this leads to a better product. By being able to select the best-in-class from each market segment, a customer gets the best possible product.

Clayton Christiansen’s evolution of the PC industry, 1978 – 1990

Source: The Innovator’s Solution, Clayton Christensen & Michael Raynor. Harvard Business School Publishing, 2003

The framework can be useful to look at solar technologies. In particular, let’s contrast the thin film value chain with the silicon value chain.

Thin film: integrated

I’ll use First Solar as the prototype for this segment. (They are being chased by a bunch of startups, but nobody else is manufacturing in the same scale.) They take in a bunch of raw materials: glass, cadmium telluride, and electrical components… and ship out a completed module. Their value chain looks more like Apple’s integrated PC model: they are a single manufacturer responsible for high efficiency, mechanical integrity, and manufacturing uniformity.

Thin Film Value Chain

Silicon: disaggregated

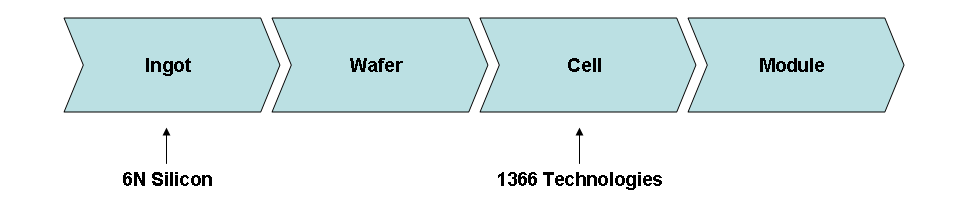

The silicon value chain is quite different. There are four discrete pieces of the value chain: silicon is refined into an ingot, then cut into a wafer, then wafers are cut up and scribed to create cells (the step that makes the material photo-active), and then assembled into modules. Each of these products has a market where they can be bought and sold.

Silicon Value Chain

Implications for market competition

Perhaps some of First Solar’s success comes from their close coordination?

Certainly, much of the cost advantage that First Solar enjoys comes from the fact that its semiconductor is thin (and therefore cheap). The bandgap of CdTe is tuned better to the wavelength of the sun’s light. However, their labor content and materials handling costs are also very low, which can only be achieved with the close coordination of manufacturing. Also, by depositing the entire semiconductor stack at once (CdTe, CdS, and the front & back electrodes), First Solar can optimize and minimize the design & materials used.

Silicon might benefit in the longer term from integrating best-in-class technologies across the value chain

Silicon’s value chain should be a long-term strength. Startups can focus on innovating within specific segments of the value chain. They don’t have to integrate vertically in order to produce & ship a product. Therefore, then, the customer will be able to assemble the best-in-class from each market segment, in order to optimize the cost & performance of silicon. A couple examples:

- 6N Silicon is developing technology with uses metallurgical-grade silicon handling for ingot production. Their approach isn’t as pure as the current methods, but the costs fall much faster than the performance does.

- 1366 Technologies is developing technologies to make the cell more efficient: thinner front contacts, a more absorptive front side of the cell, and a more reflective back side.

Both of these startups are focused on different parts of the silicon value chain (ingot and cell, respectively), and so they are not actually competing with each other. Perhaps they might both be part of the winning technology assortment.

So even though First Solar has a huge cost advantage right now, don’t count crystalline silicon out just yet. The market structure is in their favor.

The Low-Efficiency Penalty

“Dollar per watt” can be a misleading number. For those who aren’t familiar, if you sell a 150-watt module for $300, that’s $2/watt. Pretty simple.

However, even though it’s a common way to talk about pricing, it leaves a lot out of the equation. In particular, it doesn’t factor in the efficiency of the module. Lower-efficient modules require more space for the same amount of power output. That means more racking to hold them up, more labor to install them, and more land. I’ve heard people talk about a “penalty” for low efficiency, so I wanted to calculate what that would look like.

I put together a very simple model of a PV system. The PV modules, inverter, and wiring are all defined on a $/watt basis, while the racking and labor are defined on a price per square meter of solar modules. So, with lower efficiency modules, you need more of them – and the model grosses up the racking and labor in proportion.

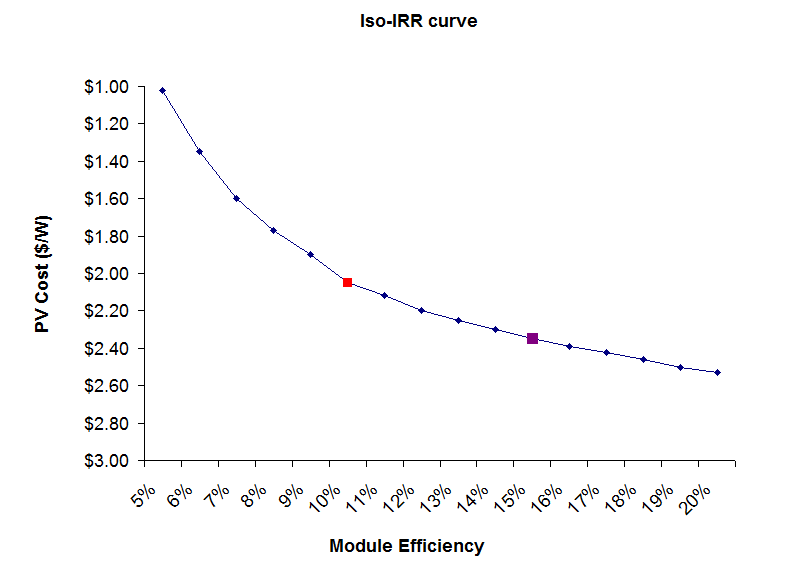

Let’s work through a quick example. With the assumptions above, a developer would earn a 10% return if he installed 1MW of 15% efficient modules while paying $2.35/watt for the modules. On the other hand, he would also earn a 10% return if he installed 1MW of 10% efficient modules, paying $2.05/watt. In other words, he needs a $0.30/watt discount for the 10% efficient panels, because he needs to use that money to buy the extra racking and pay for the extra labor.

You can plot these points on a curve. Below, I show all the points at which a developer is indifferent, for efficiencies ranging from 5% to 20%. (Note that I flipped the price axis, so that the numbers get smaller as you go up. The consulting rule of thumb is that “good” is always up and to the right, and in this case, “good” is cheap.) The two points in my example above are shown as the red and purple boxes.

The interesting here is that the curve gets steeper the further to the left you go. The difference between 20% and 15% efficiency is only $0.16/watt. Between 15% and 10% it’s $0.35/watt. Between 10% and 5%, the difference is a full $1.00/watt.

The interesting here is that the curve gets steeper the further to the left you go. The difference between 20% and 15% efficiency is only $0.16/watt. Between 15% and 10% it’s $0.35/watt. Between 10% and 5%, the difference is a full $1.00/watt.

This is a big reason why so many people are pessimistic on amorphous silicon. With expected efficiency of only around 5-7%, they start with a $0.75 to $1.33 penalty versus a silicon panel that gets 15% efficiency.

Cleantech vs IT

How Renewable Energy Is Different From Information Technology – And What That Means For Entrepreneurs

Fundamental Driver 1: In IT, the key is often finding or creating a market. In cleantech, the market is usually there; instead the key is cutting cost.

- Operational experience and ability to execute is going to be more important than creativity and the ability to anticipate demand.

- Long-term, there will be margin pressure. Since the final product is usually a commodity (electrons, or fuel), there is not as much ability for cleantech companies to achieve or sustain significant price premium.

- The market is already huge. This counters the margin pessimism in #2: while startups may not be able to increase prices, they should be able to sustain margins if they are able to dramatically reduce costs.

Fundamental Driver 2: Cleantech businesses are based on hard science, while many IT businesses are based on a concept or a customer pain

- There will be fewer garage-startups, and fewer mini-spinouts from large firms (a la employees leaving Oracle or IBM to start their own business).

- Labs, both academic and government, will be far more prominent in supplying technologies – and the ability to find & license IP will be critical for early-stage entrepreneurs.

- Landmarks are different: rather than getting customers early and iterating product & features, cleantech companies must hit laboratory technology milestones, pilot projects, and extended-life stress testing.

Fundamental Driver 3: Cleantech business require longer lead times and more money than IT

- Bootstrapping becomes much more difficult – very few companies will go from concept to IPO without private funding.

- There will also be fewer mega-wealthy entrepreneurs, because maintaining equity will be more difficult.

- Given the longer time from concept to revenue to IPO, there will be fewer serial entrepreneurs.

- There may be an opportunity for entrepreneurs to specialize in companies that are in specific stages of development (e.g. proof of concept, sales ramp-up, or manufacturing scale-up).

Fundamental Driver 4: The “Cleantech” industry is not monolithic. There is electricity generation, electricity storage, water, transportation, and energy efficiency – and each of these has 5-10 very unique sub-sectors

- In some specific industries, experience from related fields is highly valuable. Semiconductor experience is valuable for solar PV; oil & gas and biotech experience is valuable for biofuels.

- It’s sometimes more difficult for VCs to add value. Certain things transfer well: the ability to bootstrap and manage cash during rapid growth, and the ability to navigate government/regulatory issues. However, technology expertise and market knowledge don’t necessarily translate across diverse sectors.

6 comments